Modified by Simisola Fagbola, Econoday Financial Expert

The Economic situation

Monetary policy

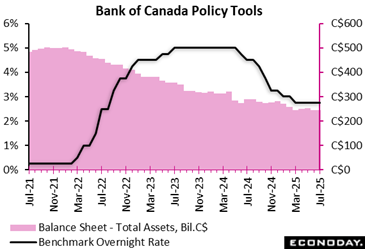

The Financial institution of Canada left its target rate of interest unmodified at 2 75 percent for the 3rd successive conference, as expected by forecasters in an Econoday study. The reserve bank cited the resilience of the Canadian economic situation and recurring pressures on core rising cost of living, adding it continues to proceed “very carefully.”

In his opening up declaration of an interview following the plan news, Guv Tiff Macklem claimed, “At this rate decision, there was clear consensus to hold our plan price unchanged.” The mins of the June meeting had actually explained “some diversity of views on the most likely course ahead”.

The impact of profession policy and related unpredictability on Canada’s financial task and inflation remains the vital component for the interest rate path forward. “If a weakening economy puts further descending pressure on rising cost of living and the upward rate pressures from the profession disruptions are consisted of, there might be a requirement for a decrease in the policy rate of interest,” the BoC stated.

It remains to keep an eye on the impact of united state tariffs on Canadian exports, exactly how this subsequently overflows to service investment, work and consumer costs. As it discussed in its June statement, the Bank also continues to analyze the level and speed at which companies pass on cost increases to customers while checking inflation expectations.

Overall, when faced with the continuous changability of U.S. profession actions regardless of some “a lot more concrete” elements in recent weeks, the central bank continues to stay clear of supplying its conventional base instance circumstance, offering 3 possible paths rather: the existing situation, a rise scenario, and a de-escalation situation.

Under the present circumstance based on tolls already in position, Canada’s GDP growth contracts in the 2nd quarter of 2025 It recoups to concerning 1 percent in the 2nd fifty percent of this year as exports maintain and home investing enhances slowly. Weakness continues next year before development gets to near 2 percent in 2027 Inflation, presently at 1 9 percent, continues to be close to 2 percent throughout the horizon as upward and downward pressures offset each various other.

Under the de-escalation situation, GDP growth rebounds much faster and rising cost of living is expected to remain below the 2 % target until late 2026 Inflation would certainly balance around 2 percent in 2027

Under the acceleration scenario, development contracts with the end of 2025 CPI rising cost of living is predicted to come to a head at just above 2 5 % in the 3rd quarter of 2026, before declining to around 2 percent in 2027

In all 3 circumstances, the neutral small price is assumed to be between 2 25 percent and 3 25 percent. At 2 75 percent, the current policy price sits at the middle of the neutral variety.

In general, the central bank left the door available to additional rate cuts to support development as lengthy as inflation can stay under control.

The BoC made its statement as uncertainty continues to be around the result of the most recent round of trade settlements. United State Head of state Donald Trump established an Aug. 1 deadline for reaching a deal, without which he stated it will certainly enforce 35 percent tolls on Canadian products. Head Of State Mark Carney has actually lately moved his messaging to indicate that some degree of tolls will continue to be.

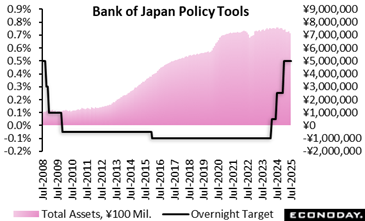

— The Financial institution of Japan’s nine-member board voted with one voice to maintain the target for the over night rate of interest at 0. 5 % for the 4th straight conference after treking it by 25 basis points (0. 25 percent point) in January amid unpredictability over profession rows.

— The bank will certainly proceed elevating rates if development and rising cost of living advance in line with its medium-term expectation yet it is still in the process of stabilizing its monetary plan stance from years of maintaining temporary rates near no percent.

— In its quarterly Expectation Report, the board left its development forecasts little altered for 2025, 2026 and 2027 (ending in March 2028 while revising up its rising cost of living overview dramatically for the current and seeing tame rate rises in monetary 2025 and 2026 as forecasted in the April record.

— The BOJ additionally kept in mind that threats to its GDP expectation is manipulated to the disadvantage, as forecasted in April, but claimed risks to its CPI forecast is “generally well balanced,” contrasted to the April statement that it was skewed to the disadvantage.

— The BOJ remains to anticipate Japan’s economy will clear up about 2 % rising cost of living. “In the second fifty percent of the estimate duration (fiscal 2025 via financial 2027, underlying CPI inflation is most likely to be at a degree that is usually consistent with the price security target, it said, duplicating its previous record released on May 1

The typical estimates by the board from its quarterly Expectation Record:

FY 25 core CPI (ex-fresh food) + 2 7 % vs. + 2 2 % in May

FY 26 core CPI (ex-fresh food) + 1 8 % vs. + 1 7 % in May

FY 27 core CPI (ex-fresh food) + 2.0% vs. + 1 9 % in May

FY 25 GDP +0. 6 % vs. +0. 5 % in May

FY 26 GDP +0. 7 % vs. +0. 7 % in May

FY 27 GDP + 1.0% vs. + 1.0% in May

— The board duplicated that “Japan’s financial development is likely to moderate” as trade and other policies lead to a downturn in abroad economic situations and to a decrease in residential company earnings despite support from accommodative financial problems. “Afterwards, Japan’s financial growth price is likely to rise, with overseas economic situations returning to a moderate development course,” it claimed.

— Board members cautioned that there are numerous threats to their expectation. “Particularly, it remains highly unpredictable exactly how trade and other plans in each territory will develop and exactly how overseas financial activity and costs will certainly react to them,” the BOJ said. “It is therefore necessary to pay due interest to the impact of these growths on financial and foreign exchange markets and on Japan’s economic activity and costs.”

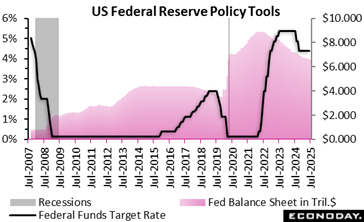

The FOMC left the fed funds target price range unmodified at 4 25 to 4 50 percent, as anticipated. There are just minor tweaks to the declaration contrasted to that released at the prior conference. The declaration noted the proceeding impact that the uncommon movements in global trade have actually carried the GDP data and provided a somewhat much less upbeat analysis of economic task. There was no adjustment in the language relating to the labor market and rising cost of living. The declaration said, “Although swings in web exports continue to impact the data, recent indicators suggest that development of economic task regulated in the initial half of the year. The joblessness rate stays low, and labor market conditions stay strong. Inflation continues to be somewhat raised.”

The statement also said, “Uncertainty concerning the financial expectation stays raised.” The language around decreased uncertainty in the previous statement was removed.

The vote at the end of the meeting consisted of two dissents from Governors Michelle Bowmand and Christopher Waller who both favored a 25 basis point cut in the fed funds rate. It is uncommon for a governor to dissent, and two governors have not dissented in a conference vote because the 1990’s. The ballot was 9 – 2 with Guv Adriana Kugler absent and not ballot.

Work

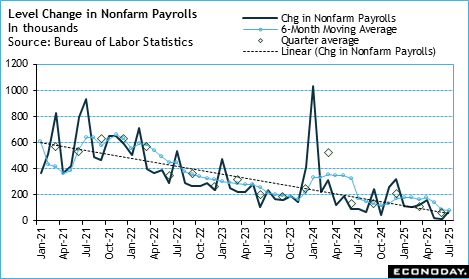

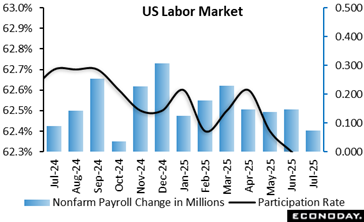

The month-to-month United States work record has substantial alterations that paint conditions in the labor market as much weaker than previously assumed and reshapes the overview for financial policy. The quick air conditioning in hiring and little rise in the unemployment rate make a rate reduced at the September 16 – 17 FOMC conference much more most likely unless the following round of rising cost of living records are particularly alarming.

Nonfarm pay-rolls are up 73, 000 in July after rises of 14, 000 in June and 19, 000 in May. July nonfarm payrolls are below the consensus of up 110, 000 in the Econoday study of forecasters. The July boost is not materially various from the 2nd quarter regular monthly average of up 64, 000, or the six-month moving standard of up 81, 000 Nonetheless, the last 3 months of hiring stands for a sudden stagnation from the fourth quarter 2024 average of up 209, 000 and first quarter 2025 standard of up 111, 000

The BLS kept in mind, “Revisions for May and June were bigger than normal. The adjustment in overall nonfarm payroll employment for May was revised down by 125, 000, from + 144, 000 to + 19, 000, and the change for June was revised down by 133, 000, from + 147, 000 to + 14, 000 With these revisions, employment in May and June incorporated is 258, 000 less than formerly reported.”

Private pay-rolls are up 83, 000 in July. Goods-producers’ payrolls are down 13, 000 with making down 11, 000 and extracting down 4, 000, while building included 2, 000 tasks. Service-providers included 96, 000 work in July, most of which are from hiring 73, 300 in health care and social support.

Government jobs are down 10, 000 in July because of declines of 12, 000 at the federal degree and 3, 000 in city government. State governing hiring is up 5, 000

Ordinary per hour earnings are up 0. 3 percent in July from June and up 3 9 percent year-over-year. Month-to-month rises in ordinary hourly earnings remain moderate and the year-over-year adjustment has been essentially the same because January.

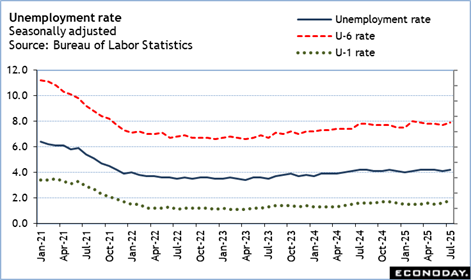

The unemployment price is up a tenth to 4 2 percent in July due to a 260, 000 decrease in the number of people utilized and a boost of 221, 000 in the variety of jobless. The U- 6 price– the widest action of joblessness– is up two-tenths go 7 9 percent in July and indicates extra workers are dissuaded concerning locating tasks.

GDP

Financial growth in the euro location cooled down a little in the 2nd quarter of 2025, with GDP bordering up by simply 0. 1 percent compared to the previous quarter, a masked comparison to the projections of minus 0. 1 percent. This marks a notable downturn from the very first quarter’s stronger 0. 6 percent growth, meaning expanding care across the bloc in the middle of persistent financial unpredictability.

Year-over-year, the economic climate kept moderate momentum, with GDP rising by 1 4 percent, a slight dip from the previous quarter’s 1 5 percent. This suggests that, while the region continues to be on a growth course, it is browsing a more vulnerable recuperation stage, reflecting financial plan and profession unpredictabilities affecting the bloc.

Within the area’s quarterly development, France increased 0. 3 percent after 0. 1 percent, while Spain grew 0. 7 percent after 0. 6 percent. Nonetheless, Germany dropped by minus 0. 1 percent after 0. 3 percent, while Italy also fell by minus 0. 1 percent after 0. 3 percent.

These updates supply an early signal that the eurozone’s recovery is still undamaged, though losing speed. The marginal quarterly gain highlights the need for caution amongst policymakers and financiers, particularly as customer confidence and financial investment view become much more critical in guiding the area’s short-term economic instructions.

U.S. economic activity rebounded in the 2nd quarter of 2025, as the substantial drop-off in products imports, coupled with a noteworthy rise in consumer spending, drove the increase in genuine GDP. Further factor for the Federal Reserve to hold off on cutting the government funds price at the final thought of the FOMC meeting today.

Q 2 GDP boosted by 3 percent, greater than offsetting the 0. 5 percent decline in the first quarter and beating expectations for a 2 5 percent increase in the Econoday survey of forecasters.

Consumer costs as gauged by Personal Usage Expenses was up 1 4 percent in Q 2 complying with simply a 0. 5 percent uptick in the very first quarter, while the need for imports dove 30 3 percent after Q 1’s 37 9 percent rise.

Nevertheless, exports were likewise down last quarter– solidifying the rise in financial activity. The decline was by 1 8 percent, cancelling out 0. 4 percent development in the first quarter. Gross domestic exclusive investment also plunged, down 15 6 percent– more than half of Q 1’s 23 8 percent dive.

United States Testimonial

Weak Jobs Report Puts Price Cut Down on Table for September

By Theresa Sheehan, Econoday Financial Expert

The July Employment Scenario provides a big drawback surprise. Not only was the 73, 000 increase in nonfarm payrolls below the Econoday agreement forecast of up 110, 000, but there was a substantial net revision lower of 258, 000 for the previous 2 months. The sub-par boost in July pay-rolls in addition to the reset to work gains in the previous 2 months alters the outlook for monetary policy.

The FOMC will certainly need to reassess the threats to maximum work, particularly if the initial benchmark revision scheduled for launch on September 9 additionally verifies that task gains are lower than formerly believed. Had the July employment data been offered on July 30, a rate cut would certainly have been virtually assured. As it is, the Fed policymakers may find the threats to rising cost of living from tolls are less compelling when they next satisfy on September 17 – 18 Of course, this will depend on the data reports set for release in the intermeeting period.

In any case, hiring has cooled down abruptly and considerably, and to the factor where it recommends that businesses are not only not employing however that they will soon be reducing current staffing.

The one-tenth uptick to 4 2 percent in the July joblessness rate is well within typical month-to-month variation. Nevertheless, it must not be dismissed out of control. In the context of the two-tenths climb in the U- 6 joblessness rate to 7 9 percent, it seems like the start of an upward pattern. The unemployment rate has actually fixed at 4 2 percent in four of the past five months and is at the top of the slim variety of 4.0 percent to 4 2 percent that has actually prevailed for the previous 20 months.

It is likewise noteworthy that the joblessness rate for those jobless 15 weeks or longer depends on 1 8 percent in July after 1 6 percent in June and 1 5 percent in May. Periods of unemployment are lengthening.